For years, C-suite executives at health plans viewed value-based care (VBC) as an idealistic evolution - a long-term shift from volume to value that could be phased in via gentle, upside-only pilots. It was a line item managed by population health teams, decoupled from the core actuarial and underwriting engines that drive premium pricing.

That pilot era is officially dead. Today, health plans face an unprecedented financial squeeze. According to updated data from PwC’s Health Industries practice, commercial medical cost increase trends have been restated upward to a staggering 9.0% growth for commercial group plans and 8.5% for individual markets. Compounding this, the Milliman Medical Index (MMI) reports that employer-sponsored healthcare costs grew by 7.9% year-over-year, marking the highest baseline cost increase in more than a decade.

With commercial group enrollment flattening and Medicare Advantage (MA) margins facing severe compression from finalized regulatory changes, including structural adjustments to the CMS risk adjustment models and stricter Star Ratings criteria—health plan executives can no longer rely on standard unit-cost discounts or aggressive prior authorization to sustain financial viability. Value-based care has transformed from a clinical quality initiative into a core survival strategy for the balance sheet.

1. The Macro Economic Forces Rewriting the Rules

To understand why traditional fee-for-service (FFS) contracting has broken down, executive leadership must look at the specific macro drivers inflating claims spend. The current inflationary cycle is not driven by simple utilization volume; it is driven by complex structural shifts in provider behavior, therapeutic innovations, and regulatory updates.

A. The Provider AI Arms Race and "Coding Inflation"

One of the most insidious cost drivers in the commercial market is the rapid provider adoption of AI-enabled documentation and coding tools. Nearly 70% of health plans surveyed by PwC ranked these tools as a top three cost inflator.

Providers are using generative AI to scan electronic health records (EHR) and instantly capture greater clinical specificity and reimbursable severity. The result? Payers are seeing higher paid amounts per claim driven entirely by shifts in documentation rather than any actual change in patient complexity. Traditional FFS contracts have no systemic defense against this artificial coding intensity; only value-based structures that reward holistic patient outcomes can insulate a payer from automated bill-maximized coding.

B. The Pharmacy and GLP-1 Imperative

Pharmacy expenditure has become the fastest-growing component of commercial healthcare costs, rising 14.8% year-over-year for the average individual. This spike is anchored by a near-doubling of glucagon-like peptide-1 (GLP-1) receptor agonist prescriptions (such as Ozempic and Wegovy) filled over a 12-month period.

With list prices easily exceeding $1,000 per month and indications expanding rapidly into cardiovascular risk reduction, traditional utilization management (UM) and restrictive prior authorizations are failing to stem the tide. FFS models offer no financial protection against these chronic, high-cost maintenance therapies. Payers must transition accountability for long-term pharmaceutical appropriateness and return on investment (ROI) directly to risk-bearing provider groups via total-cost-of-care (TCOC) models.

C. The "Digital Quality" Regulatory Mandates

Federally, the timeline is unyielding. The Centers for Medicare & Medicaid Services (CMS) maintains its strict mandate to have 100% Traditional Medicare beneficiaries and most of the Medicaid enrollees in accountable care relationships by 2030.

Concurrently, the National Committee for Quality Assurance (NCQA) is accelerating its transition to purely digital quality measures (dQMs), actively retiring manual chart reviews in favor of automated, FHIR-based (Fast Healthcare Interoperability Resources) data streams. Plans that fail to build the data infrastructure required to ingest, validate, and trade digital clinical insights with providers will not only lose their value-based margins; they will face catastrophic hits to their quality ratings and market access.

2. Moving From "Upside Shared Savings" to True Risk Alignment

Many health plans claim they have robust VBC penetration because a high percentage of their network is tied to an Alternative Payment Model (APM). However, looking under the hood often reveals that most of these contracts are upside-only shared savings arrangements. In these models, providers share financial savings if they beat a benchmark but face no penalty if they exceed it.

This asymmetric risk profile no longer works for payers. Upside-only agreements create a "heads you win, tails I lose" dynamic that fails to drive meaningful provider behavior modification or structural cost reduction. True risk alignment requires an intentional transition to two-sided financial accountability.

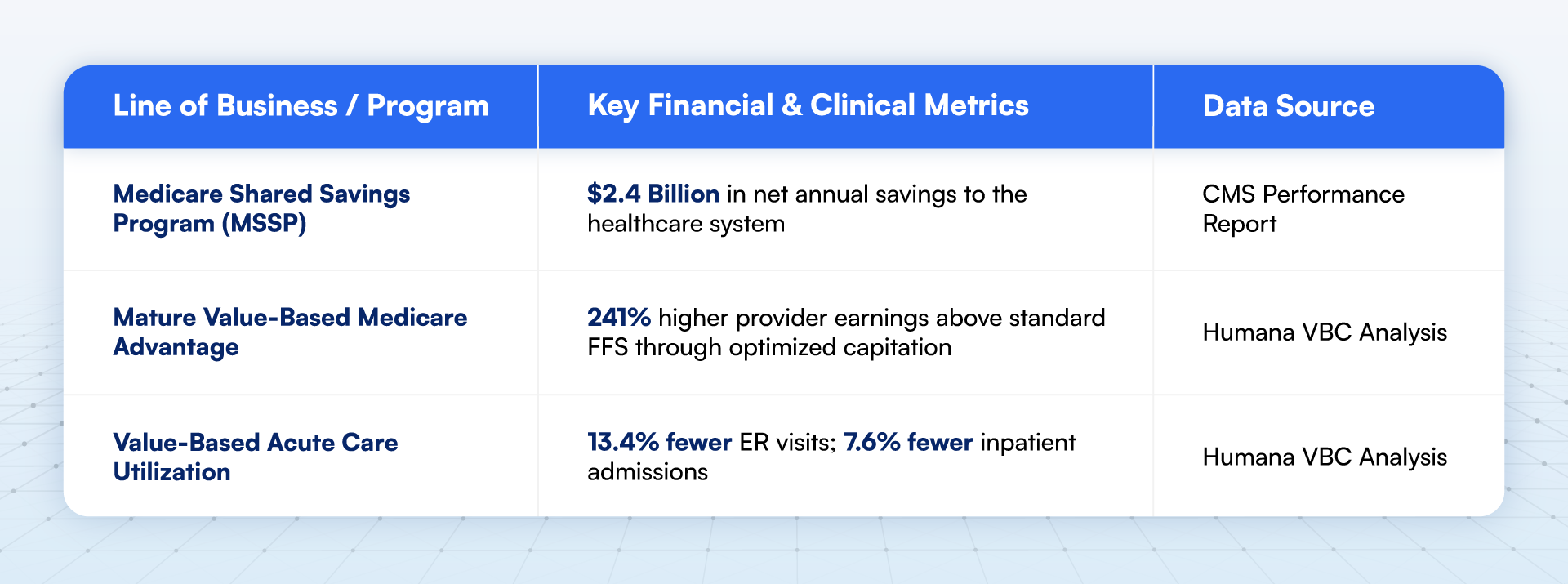

The data proves that structured, two-sided risk delivers the macro-level savings that health plan CFOs require:

Despite these clear benefits, plans frequently encounter provider resistance when trying to implement downside risk. Data from the National Association of ACOs (NAACOS) indicates that 87% of healthcare organizations identify financial downside liability as their primary barrier to VBC adoption. Providers are hesitant to accept downside risk because they feel they lack the data transparency and operational tools required to manage it.

To break this impasse, advanced health plans are shifting their strategies. Rather than forcing providers into standard capitation models, plans are acting as data enablers—providing the financial backstops, predictive analytics, and point-of-care infrastructure necessary to make downside risk manageable for provider organizations.

3. The Blueprint for Executive Action

To transition value-based care from a marketing tagline to an operational margin strategy, health plan executives must modernize the technical and financial connection between the payer and the provider.

The multi-year corporate strategy for health plans should focus on three foundational capabilities:

A. Real-Time Interoperability and Automated Payment Integrity

Historically, plans and providers looked at healthcare data through completely different lenses. Plans relied on retrospective claims data that was typically 60 to 90 days old, while providers operated on immediate but siloed EHR data. Trying to run a downside-risk contract on 90-day-old claims data is like trying to drive a car by looking solely in the rearview mirror.

Health plans must invest heavily in deploying bi-directional FHIR APIs that connect directly into provider workflows. Instead of sending monthly Excel spreadsheets detailing gaps-in-care, plans must push real-time alerts into the EHR at the exact moment a clinician is seeing a patient.

Furthermore, to counter the AI-driven "coding inflation" mentioned earlier, plans must integrate their contracting engines with advanced, prospective coding surveillance tools. By monitoring provider-level severity drift and documentation variations before payments are disbursed, plans can ensure payment accuracy based on true patient complexity rather than optimized documentation.

B. Scalable Specialist Engagement and Episode-Based Bundles

For the past decade, VBC has been largely synonymous with primary care optimization. While advanced primary care is critical for managing chronic conditions, primary care physicians directly control only a fraction of total medical expenses. Most of the acute, high-cost claims are driven by specialists.

Total health plan spend is ~10-15% related to primary care and 85-90% related to specialist & accurate care. The specialist & acute care is the next frontier for VBC strategy.

Health plan leaders must aggressively expand their value-based frameworks into specialty care, targeting high-volume, highly variable specialties:

- Cardiology: Implementing bundles for congestive heart failure (CHF) management and coronary artery disease, tying payments to the avoidance of 30-day readmissions.

- Oncology: Shifting from FFS drug-reimbursement markups to comprehensive oncology care models that incentivize adherence to clinical pathways and reward the reduction of emergency department visits during active chemotherapy.

- Orthopedics: Moving major joint replacements (hip and knee arthroplasty) completely into prospective bundled payment models that cover the pre-operative, surgical, and 90-day post-acute care windows.

By focusing on these specific clinical episodes, plans can address the 85-90% of total medical spend that sits outside the traditional primary care medical home.

C. Predictive Risk Stratification and Event-Driven Care Management

Traditional care management programs are notoriously inefficient. They frequently rely on retrospective analyses that identify "high utilizers" after they have already completed their expensive hospital stays. By the time a care manager calls the member, the clinical and financial damage is already reflected in the claims run out.

Advanced VBC demands a pivot to event-driven, predictive care management. By using machine learning models that blend historical claims, real-time admission-discharge-transfer (ADT) feeds, and hyper-local Social Determinants of Health (SDoH) data (such as housing stability and transportation access), plans can identify members at high risk for decompensation before an acute event occurs.

Crucially, corporate leadership must stop funding general care management programs that cannot demonstrate clear, avoided utilization or verifiable actuarial savings. Every care management lever must have an explicit trend-deflation target attached to it.

4. Operationalizing the VBC Blueprint: A Step-by-Step Transition

For health plan leadership, the challenge is rarely understanding the theory of VBC—it is executing the transition without disrupting current revenue streams or alienating core provider networks. Moving an organization from a legacy fee-for-service infrastructure to an integrated value-based ecosystem requires a disciplined, step-by-step approach.

A. Establish the Data Baseline and Transparency (Months 1–6)

Before amending a single provider contract, plans must align claims data with provider EHR data. Deploy FHIR-based data pipelines to ingest clinical feeds and eliminate the 60-day claims lag. Share these unified baselines with your top 20% tier-one provider groups to build actuarial trust.

B. Introduce Class-Specific Specialty Bundles (Months 6–12)

Shift high-volume, predictable acute procedures (e.g., total joint replacements, routine cardiology episodes) out of open-ended FFS. Implement fixed, prospective bundled payments with historical quality benchmarks to immediately capture low-hanging specialist savings.

C. Transition Primary Care to Two-Sided Risk Corridors (Months 12–18)

Migrate mature, upside-only primary care networks into symmetrical two-sided risk agreements. Introduce financial downside guardrails (e.g., a minimum loss ratio corridor) combined with real-time care-gap alerts within the EHR to protect providers while demanding accountability.

D. Implement Predictive AI Care Management and Global Capitation (Months 18–36)

Deploy machine learning models that combine clinical, SDoH, and pharmacy data to flag rising-risk members before hospitalization occurs. For advanced, highly aligned provider systems, transition fully to global capitated or total-cost-of-care (TCOC) contracts, transferring complete premium accountability to the delivery system.

The Bottom Line

The macroeconomic numbers confronting health plan executives in the current environment do not leave room for administrative inertia. With a 9.0% annual commercial cost increase trend, a spike in hospital inflation to 7.59%, and regulatory pressure squeezing Medicare Advantage and Medicaid managed care lines, the traditional payer playbooks have reached their structural limits.

The competitive advantage now belongs entirely to the health plans that can move past the administrative friction of processing transactional claims and and use AI to improve outcomes, reduce costs and build integrated, risk-bearing networks.

As health plan leaders refine their multi-year corporate strategies, the mandate from the market is clear: Stop treating value-based care as an isolated clinical experiment or a regulatory compliance task. Treat it as the core financial operating system required to protect your margins, deliver predictable pricing to employer groups, and secure long-term capital sustainability.